GENIUS Act Passed, How Should We Cautiously Approach the Stablecoin Narrative?

分享到朋友或朋友圈

Early this morning Beijing time, the U.S. House of Representatives passed three crypto-related legislations: the 'CLARITY Act', the 'GENIUS Act', and the 'Anti-CBDC Surveillance State Act'. Among them, the 'GENIUS Act' is expected to be signed into law by Trump this Friday local time.

This not only marks the first time the U.S. has established a national-level regulatory framework for stablecoins but also sends a clear signal that stablecoins are moving out of the gray area and into the fringes of the mainstream financial system. Meanwhile, major financial centers like Hong Kong, China, and the EU are also accelerating their pace, indicating a reshaping of the global stablecoin landscape.

Looking back over the past few months, we can see that stablecoins have almost overnight transformed from a financial variable under regulatory scrutiny into a new infrastructure officially recognized. What exactly has happened behind this, and who is pushing stablecoins to become the new protagonist on the global financial stage? How should we rationally understand this wave of enthusiasm?

From Web3 Narrative to National Strategy, Who is Pushing?

Since the beginning of the year, stablecoins have undoubtedly become the focus of global financial policy and narrative.

But this wave of enthusiasm is not accidental, nor is it the product of natural technological evolution. Instead, it is a structural shift driven by policy forces, especially the policy shift during the Trump era, which has played a highly disruptive 'catfish role'.

On one hand, Trump has always been clearly opposed to central bank digital currencies (CBDC), explicitly supporting a market-led digital dollar route. On the other hand, from endorsing the USD1 launched by family businesses to promoting and soon signing the GENIUS Act, Trump is also personally fulfilling his campaign promises to deregulate the crypto market.

This series of signals has directly forced global regulators to start re-examining stablecoins. Therefore, within just a few months, stablecoins have gone from being a marginal issue in the crypto circle to a key discussion point at the national strategic level. Apart from Hong Kong, China finalizing the implementation timetable for the 'Stablecoin Ordinance', major global economies have also begun to seriously consider and accelerate the establishment of clear compliance frameworks for stablecoins:

The EU's 'MiCA Regulation' (Markets in Crypto-Assets), which came into effect in 2024, comprehensively covers the compliance regulation of crypto assets, with detailed classifications for stablecoins;

The ruling party of South Korea's new President Lee Jae-myung proposed the 'Digital Asset Basic Act', clearly stipulating that as long as a South Korean company has at least 5 billion won (approximately $370,000) in capital and ensures refunds through reserves, it can issue stablecoins;

Objectively speaking, the passage of the GENIUS Act is not just a deregulation of stablecoins by the U.S., but also a clear choice for the digital dollar route—abandoning central bank digital currencies (CBDC) and supporting compliant, privately issued dollar stablecoins.

It can be foreseen that this U.S. stance will become a reference paradigm for other countries' regulatory designs, pushing stablecoins into the general discussion framework of global financial policies.

The Path of Stablecoins is Changing

Over the past few years, the stablecoin market landscape has long been dominated by Tether (USDT) and Circle (USDC), representing two paths: 'circulation efficiency' and 'compliance transparency':

USDT focuses on cross-platform circulation and matching efficiency, dominating in exchanges and gray settlement networks;

USDC emphasizes asset compliance and transparency, deeply cultivating regulation-friendly scenarios and institutional customer systems;

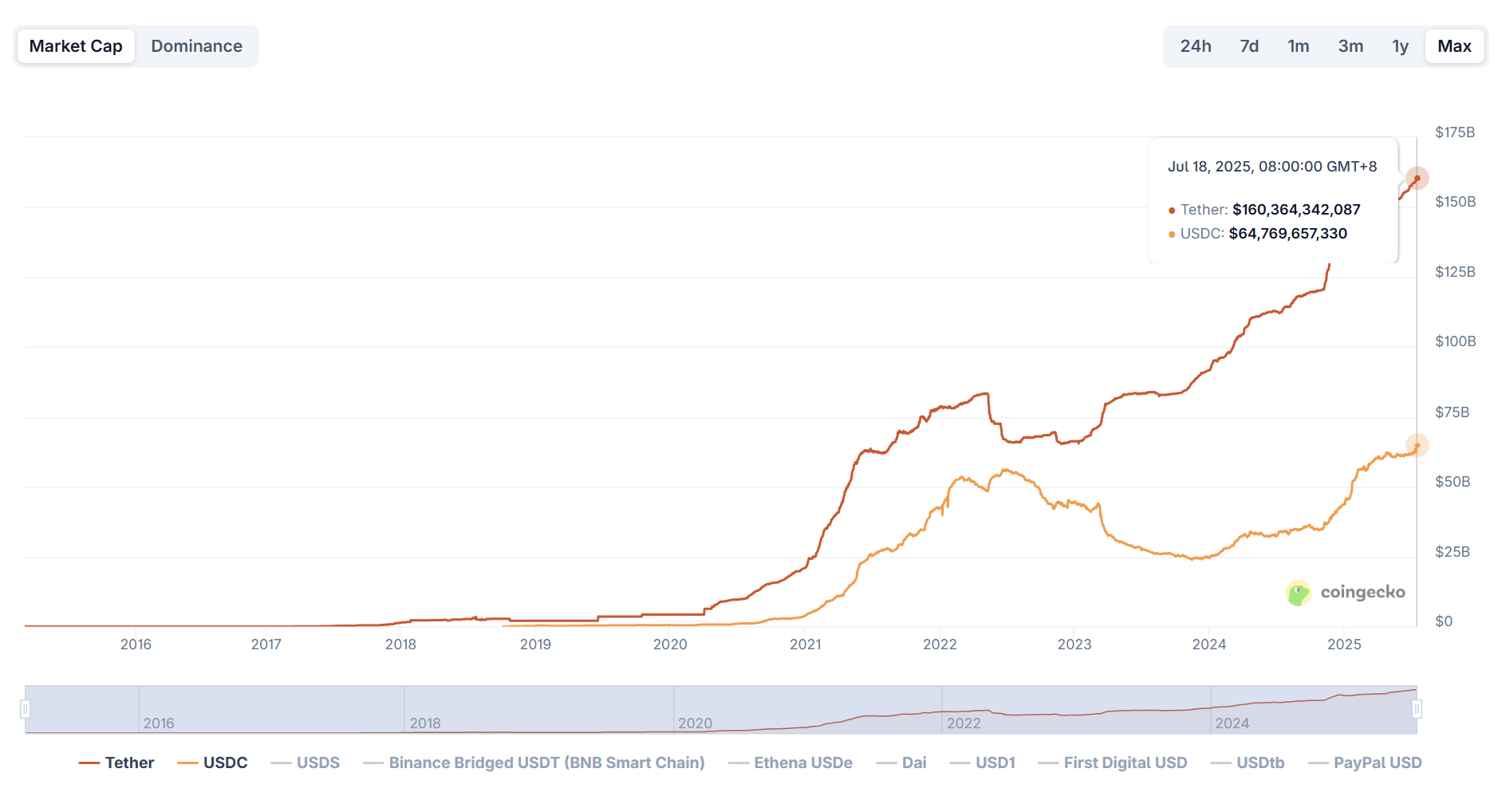

In terms of overall scale, stablecoins have maintained a growth trend since 2025—according to CoinGecko data, as of July 18, the total market value of stablecoins across the network is approximately $262 billion, an increase of over 20% compared to the beginning of the year.

This also means that in the process of the crypto market warming up, stablecoins remain the most core 'liquidity entry', with the duopoly of USDT and USDC still solid—USDT's total market value exceeds $160 billion, accounting for over 60%; USDC remains around $65 billion, accounting for about 25%, with the two combined accounting for nearly 90%.

Since 2024, more and more Web2 financial enterprises and traditional capital forces have begun to enter the field, using stablecoins to build on-chain settlement tools. For example, PayPal's PYUSD and the newly politically backed USD1 are two representative signals:

PYUSD (PayPal USD) was launched by the payment giant PayPal, naturally possessing cross-border settlement scenarios and a global merchant network; USD1 aims at on-chain compliant deposits and withdrawals and cross-border business, supported by political and business resources endorsed by Trump, targeting corporate settlement scenarios.

It can be said that with the support of institutions and national forces, these emerging stablecoin projects are transforming the function of stablecoins from 'Web3 liquidity tools' to value bridges connecting Web3 and the real economic system, and their usage scenarios are gradually expanding from exchanges and wallets into supply chain finance, cross-border trade, freelancer settlements, OTC scenarios, and other diverse uses.

Behind the Frenzy, What Are the Real Challenges for Stablecoins?

However, objectively speaking, while the GENIUS Act has granted stablecoins institutional recognition, it has also brought more compliance requirements, setting clearer boundaries for their development.

For example, issuers must undergo KYC/AML management, funds must have custody isolation and third-party audits, and in extreme cases, issuance quotas or usage restrictions may be set. This means that stablecoins have gained legal status but have officially entered the role of 'regulated currency'.

From this perspective, whether stablecoins can break through the label application restrictions of Web3 in the future is the key to achieving incremental landing. After all, looking further, the greatest growth potential of stablecoins does not lie within the internal layers of Crypto, but in the broader Web2 and global real economy.

Just like the main increments of USDT and USDC no longer come from on-chain interaction users, but from small and medium-sized enterprises and individual merchants with strong cross-border settlement needs, emerging markets and financially disadvantaged regions unable to access the SWIFT network, residents of inflation countries eager to escape local currency fluctuations, content creators and freelancers unable to use PayPal or Stripe, etc.

In other words, its future greatest increment is not in Web3, but in Web2—the real killer application of stablecoins is not 'the next DeFi protocol', but 'replacing traditional dollar accounts'.

This also means that once stablecoins become the fundamental carrier of digital dollars globally, they will inevitably touch on sensitive nerves such as monetary sovereignty, financial sanctions, and geopolitical order.

Therefore, the next phase of stablecoin growth will inevitably be closely related to the new landscape of dollar globalization and will become a new battlefield among governments, international institutions, and financial giants.

Final Thoughts

The essence of currency issuance has always been an extension of power, relying not only on asset reserves and clearing efficiency but also on national credit, regulatory approval, and international status endorsement.

Stablecoins are no exception. If they truly want to penetrate from the Crypto world into the real economic system, relying solely on market mechanisms or business logic is ultimately insufficient. Therefore, the compliance assistance brought by the global policy shift in 2025 is undoubtedly an important driver for stablecoins to move towards the mainstream, but it also means they will have to survive in more complex games.

This is a long-term game, and we are at the stage where it truly begins.