The real reason behind the collective unstaking of $1.9 billion ETH is...

分享到朋友或朋友圈

Original text from Galaxy

Compiled by|Odaily Planet Daily Golem(@web3_golem)

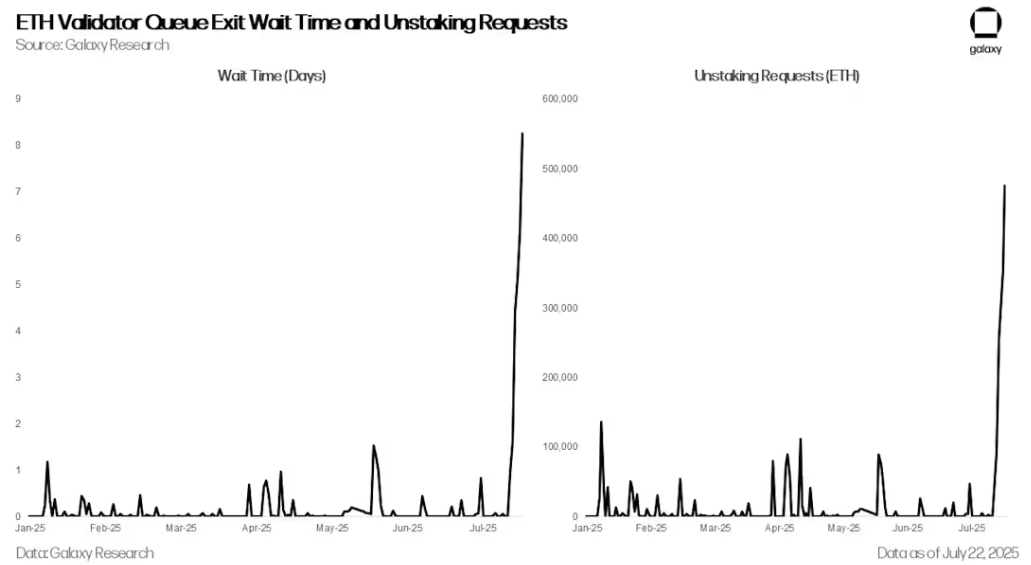

Starting from July 16, the number of ETH unstaking requests has increased sharply, with the number of validators in the exit queue soaring from 1,920 to over 475,000 by July 22, and the waiting time increasing from less than an hour to over eight days. Although the increase in unstaking activity was expected due to ETH's recent excellent price performance and the adjustment of validator staking requirements in the recent ETH Pectra upgrade, the sharp spike was mainly caused by the surge in ETH lending rates starting from July 16. The surge in rates triggered widespread liquidation of ETH loop lending strategies, which in turn exacerbated the decoupling pressure on ETH-based liquid staking and restaking tokens (LST and LRT).

ETH validator queue exit waiting time and unstaking requests

Ethereum Staking Queue

Ethereum's staking exit queue is a built-in mechanism designed to manage the orderly withdrawal of staked funds by validators from the network. To maintain network stability and prevent large-scale validator exits from jeopardizing consensus, Ethereum limits the number of validators that can exit per cycle (epoch). This limit is called the churn limit, which varies with the total number of active validators, allowing approximately 8 to 10 validators to exit per cycle (about every 6.4 minutes). When validators initiate a voluntary exit, they enter a queue and must wait their turn to be processed. After exiting, there is a waiting period (about 27 hours) before funds can be withdrawn. During periods of high exit demand, the queue can become severely congested, leading to waiting times of several days or even weeks.

This week is not the first time Ethereum has experienced a backlog of unstaking. In January 2024, due to the restructuring of the bankrupt cryptocurrency lending institution Celsius, which needed to withdraw 550,000 ETH, the queue waiting time was as long as six days.

wallet making large withdrawals from the platform. Starting from June 18, this wallet withdrew over 167,000 ETH. The sudden decrease in ETH deposits put pressure on users running ETH loop lending strategies on Aave, also leading to a surge in some redemption requests.

Loop lending strategies are widely used by cryptocurrency traders to enhance ETH staking yields. A common form is that users deposit liquid staking tokens (LST) or liquid restaking tokens (LRT) as collateral on platforms like Aave, borrow ETH, then exchange it back to LST and redeposit, repeating the process to accumulate leveraged exposure. When the staking yield exceeds the ETH lending rate, the strategy becomes profitable, allowing users to earn the interest rate spread. The strategy can be executed manually or through automated vaults provided by protocols like EtherFi and Instadapp.

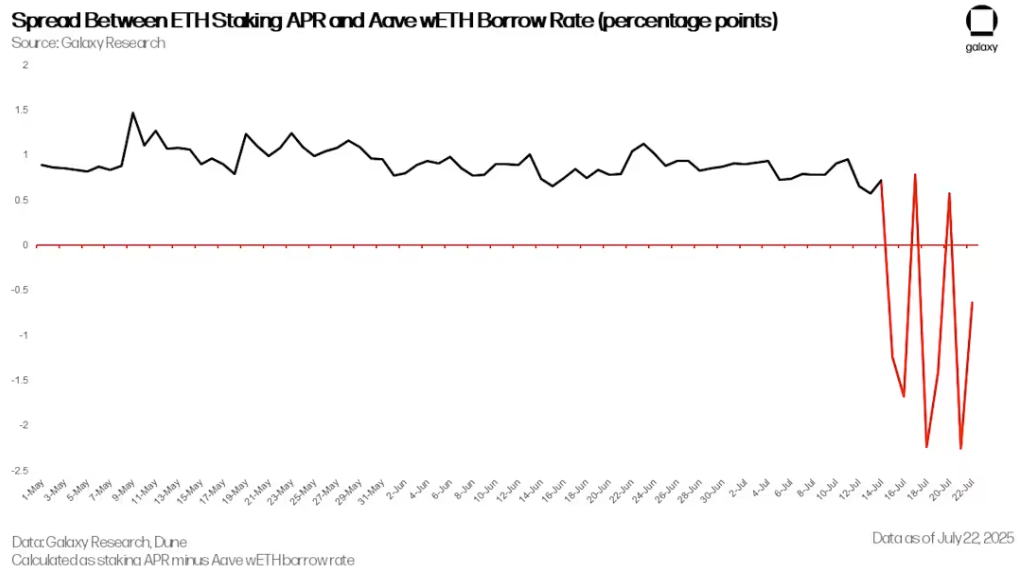

Spread between ETH staking annual rate and Aave wETH lending rate (percentage points)

However, after the ETH supply crunch starting from July 16, the spread between staking yields and ETH borrowing costs turned negative. By July 21, the spread had fallen to -2.25%, making the strategy unprofitable. This triggered collective liquidation by traders, with users starting to withdraw their provided ETH, repay loans, and gradually reduce leverage. Since many traders used LST or LRT as collateral, they needed to exchange these assets back to ETH or unstake them. This put further pressure on the LST/LRT secondary markets and the Ethereum validator exit queue.

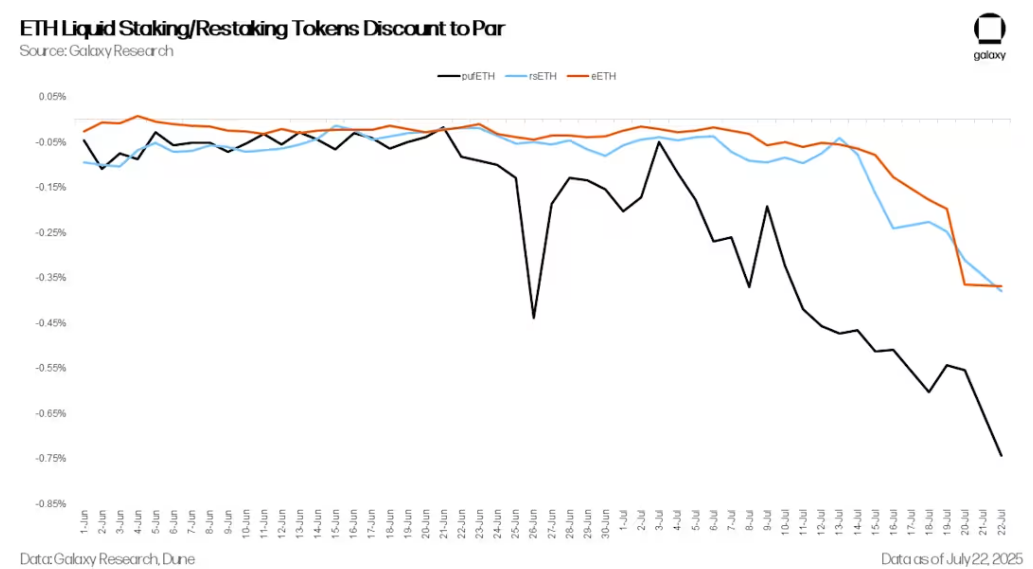

ETH liquid staking/restaking tokens below par value

As lending rates climbed, LST and LRT began to decouple further from ETH. LST/LRTs typically trade slightly below ETH to compensate for redemption delays caused by Ethereum's exit queue, limited DEX liquidity, and protocol-specific risks (such as slashing or smart contract risks). During forced deleveraging or redemption periods, this selling pressure pushes LST/LRT prices further below par value. Additionally, automated loop lending vaults reacted differently to the disruption. Some chose to unstake, while others sold directly on the secondary market. For example, as of today, EtherFi's Liquid strategy has about 20,000 ETH in the Ethereum exit queue.

Further exacerbating the queue congestion, some market participants began arbitraging the LST/LRT decoupling. By purchasing LST/LRT at a discount on the secondary market and redeeming them for ETH's full value through collateral, they could earn the spread between the two. This led to a surge in ETH exit queue requests.

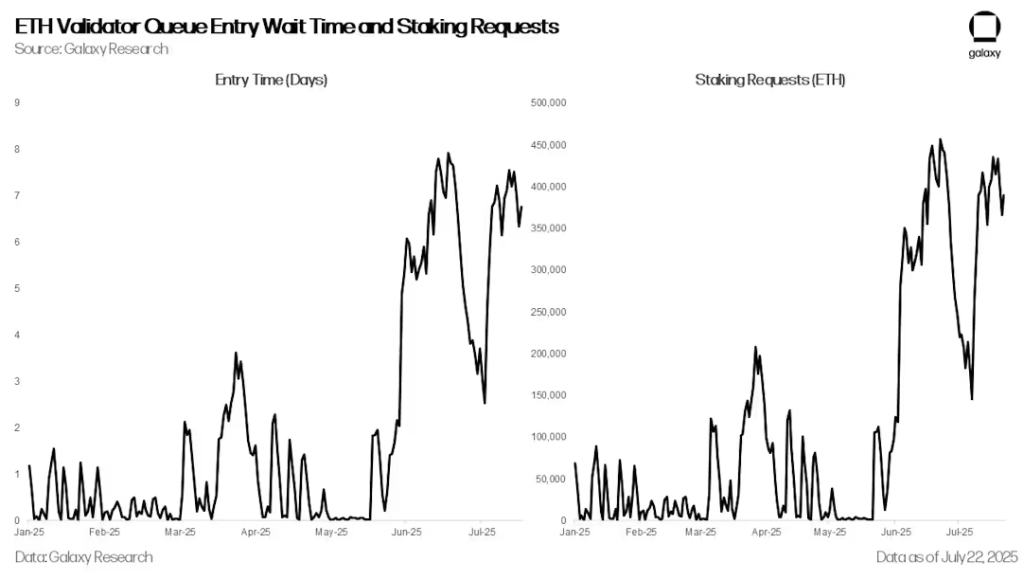

The length of the validator queue has risen to its highest level since April 2024.

Outlook

While the overall data on unstaked ETH might initially suggest a wave of profit-taking, a closer look reveals that most of the activity was driven by volatility in the ETH lending market and the sharp rise in lending rates starting from July 16. Meanwhile new staking demand remains strong, almost offsetting the ongoing withdrawals, so investors need not panic.

Despite the increased demand, ETH's staking architecture is functioning as intended. While some may complain about the significant increase in queue times, this is a feature of the network, not a flaw. It is designed to limit the speed at which validators can enter or exit, thereby protecting the stability and security of Ethereum's Proof of Stake (PoS) consensus mechanism.

However, this event highlights the ongoing fragility of the ETH liquid staking and restaking ecosystem. These assets remain sensitive to leveraged strategies and are prone to stress under extreme market conditions. The widespread impact of LST/LRT decoupling and redemption delays underscores the importance of considering term risk and liquidity bottlenecks.

Looking ahead, protocols relying solely on Ethereum's native exit mechanism may face stricter scrutiny. We anticipate growing interest in solutions that enhance redemption flexibility, such as peer-to-peer exit markets, improved LST/LRT automated market makers (AMMs), and protocol-native liquidity vaults designed to alleviate exit queue congestion and smooth fund flows.