ETH vs SOL: The 2025 Crypto War, Trillion Capital Bets on the New vs Old Order

分享到朋友或朋友圈

Original | Odaily Planet Daily (@OdailyChina)

Author | Ethan (@ethanzhang_web3)

"2021 was the year of Layer 1 competition, 2024 was the carnival of Meme. So, where will the market's main line go in 2025?"

This hotly debated question on platform X is being clearly answered by mainstream capital: with the successful legislation of the GENIUS Act and stablecoins officially incorporated into the U.S. sovereign regulatory framework, a new multi-dimensional financial narrative combining "stablecoins × RWA × ETF × DeFi" is strongly emerging.

In this profound evolution of cross-chain finance, the core focus is no longer on Bitcoin or Meme coins, but on the battle between Ethereum and Solana over the new vs old order. The two public chains have fundamental differences in technical architecture, compliance strategies, scaling paths, ecosystem construction models, and even value foundations.

Currently, this competition, which will determine the future landscape, has entered a critical stage where capital is fiercely betting with real money.

Capital Betting Preferences: From "BTC Faith" to "ETH/SOL Either-Or"

Unlike previous crypto bull markets driven by macro monetary policies with universal rises and falls, the 2025 market shows obvious structural differentiation.Leading projects are no longer rising in sync; funds are concentrating on selected battlefields, showing a survival of the fittest trend.

The most intuitive signal comes from changes in institutional buying strategies:

On July 22, GameSquare announced an increase in its digital asset treasury authorization to $250 million, adding 8,351 ETH, with the clear goal of "allocating high-quality Ethereum ecosystem assets to achieve stablecoin yields";

SharpLink Gaming accumulated an increase of 19,084 ETH this month, with total holdings reaching 340,000, worth over $1.2 billion;

A new wallet address bought over 106,000 ETH through FalconX in the past 4 days, worth nearly $400 million;

The Ether Machine announced plans to complete a backdoor listing with 400,000 ETH, receiving over $1.5 billion in financing support from top institutions including Consensys co-founders, Pantera, and Kraken, aiming to become the "largest public ETH production company".(Also recommended reading: "The Birth of a 400,000 ETH Whale! The Countdown to Approval of The Ether Machine, the First Ethereum Asset Management Platform on the U.S. Stock Market")

On the SOL side: The buying scale is equally astonishing, with a more explosive speculative nature.

Listed company DeFi Development Corp announced an increase of 141,383 SOL, with total holdings approaching 1 million;

SOL treasury company Upexi announced the purchase of 100,000 SOL for $17.7 million, with total holdings reaching 1.82 million, floating profits exceeding $58 million;

According to CoinGecko data, PENGU's market cap has reached $2.785 billion, surpassing BONK ($2.701 billion), becoming the largest Meme coin by market cap in the Solana ecosystem.

These phenomena indicate that ETH and SOL have become the preferred underlying assets for institutional multi-asset allocation. However, their investment logics show significant differences: ETH is used as "on-chain treasury high-quality asset base institutional target for spot ETF access";SOL is being shaped into "high-performance consumer application chain main battlefield of the new Meme economy".

The two betting methods represent expectations for two main lines in the future of the crypto market: ETH is the financial engine taken over by institutions, SOL is the speculative track for capital's aggressive bets.

Over the past two years, Ethereum's narrative once fell into "idling" doubts. From post-merger staking yields not significantly improving, to Layer 2 ecosystem fragmentation, high Gas fees, to projects like dYdX and Celestia actively migrating out, market expectations for ETH once hit a low.

But the reality is: ETH has never left; instead, it has become the core asset most deeply bound to institutional narratives. Its underlying support lies in deep institutional synergy across three dimensions:

Establishment of RWA Core Hub Status

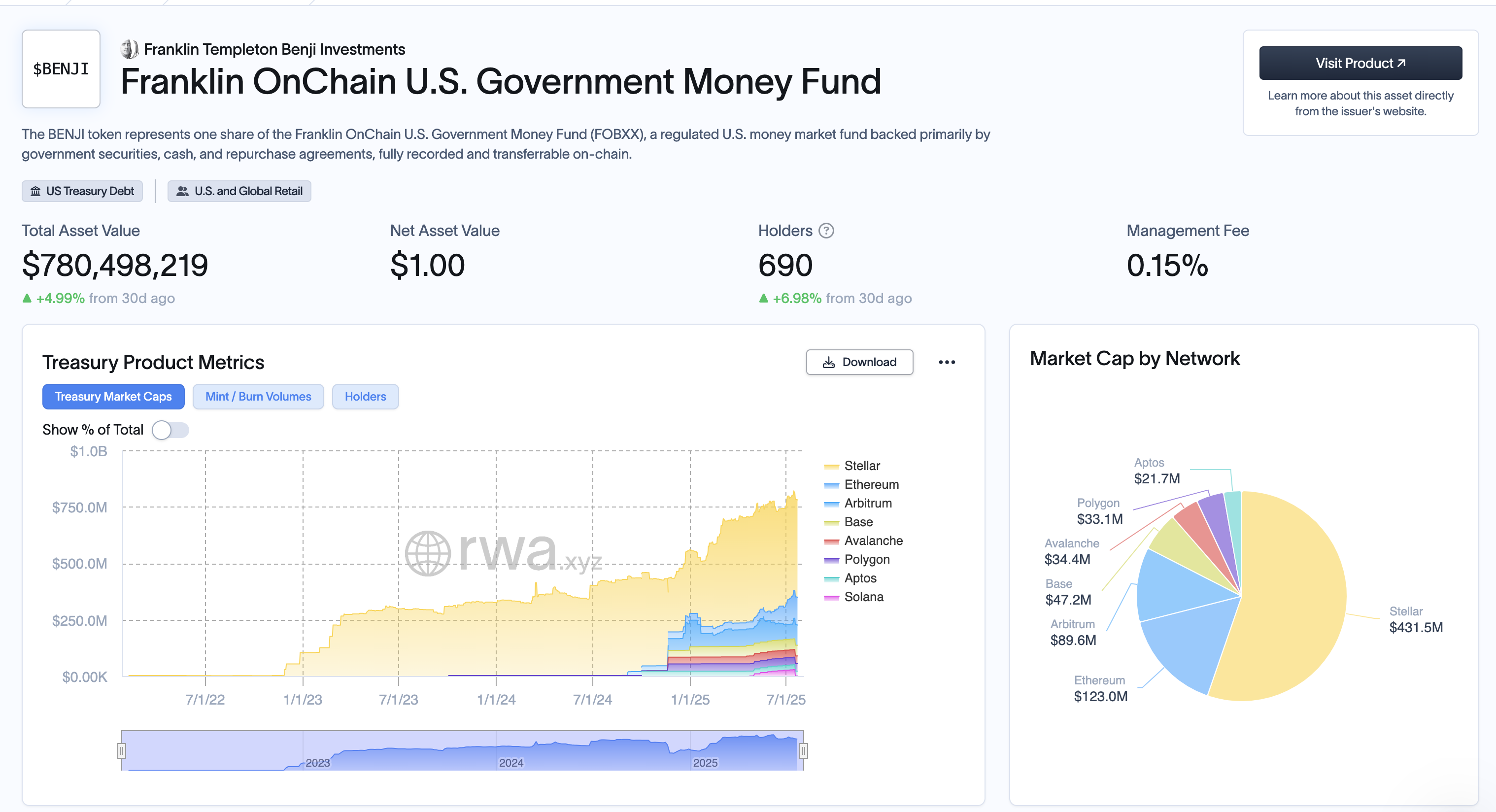

The current total RWA issued on-chain exceeds $4 billion, with over 70% occurring on the Ethereum mainnet and its L2 networks. Core products including BlackRock's BUIDL, Franklin Templeton's BENJI, Ondo's USDY, and Maple's cash funds all use ETH as a key linkage layer or liquidity medium (e.g., WETH). The larger the RWA scale, the more indispensable ETH becomes.

After the passage of the GENIUS Act, stablecoin issuers like Circle and Paxos have clearly stated "on-chain reserve transparency" and "short-term U.S. Treasury bond pledge structure" as core demands. In Circle's latest asset allocation, WETH's proportion has risen to 6.7%. Meanwhile, institutions like Grayscale and VanEck are accelerating preparations for Ethereum spot ETF products. Following BTC, ETH is highly likely to become the next ETF focus.

As of July 22, the total TVL of the Ethereum mainnet and L2 networks is as high as $110 billion, accounting for 61% of the global crypto TVL. ETH developers' monthly active users are stable at over 50,000, four times that of Solana and eight times that of other L1s. This means that no matter how market narratives change, ETH's institutional foundation and ecosystem stickiness as the "main financial layer" for on-chain asset governance, value sedimentation, and liquidity distribution are difficult to shake in the short term.

In terms of price, ETH is approaching the $4,000 mark. With BTC breaking through and stabilizing above $120,000, the process of ETH reigniting market expectations is not about creating new stories, but rediscovering old values.

Compared to Ethereum's "financial hub" positioning, Solana is more like consumer infrastructure in high-frequency scenarios. Its narrative has successfully transformed from "the chain with the best technical parameters" to "the machine for creating on-chain native hits", achieving structural breakthroughs in 2024-2025.

MemeCoin's Local Market, Not Secondary Transfer:

In this round of "crypto consumer goods" boom, the number and liquidity of MemeCoins emerging on Solana have hit record highs. Market data shows that as of July 22, Solana's highest market cap Meme project BONK reached $2.67 billion, followed by PENGU ($2.32 billion) and TRUMP ($2.2 billion), with the combined market cap of the three surpassing Dogecoin. With Solana's extremely low Gas fees and high TPS, these projects have formed a fast closed loop of "low-cost experimentation → community-driven FOMO → high-frequency trading stimulation". On Solana, Meme has become the native consumer behavior of on-chain users.

Capital Bets on "On-Chain Activity", Not Technical Routes:

The massive increases by listed companies like DeFi Development Corp and Upexi show that mainstream capital is viewing SOL as a trinity of "tradable asset user growth indicator narrative carrier", focusing on ecosystem activity, trading depth, and the consumer attributes of "on-chain stories", rather than technical details.

Ecosystem Products Move from Hits to "Basic Consumption Layer":

From Jupiter's DEX experience, Backpack mobile wallet, to Solana phones and the upcoming Solana App Store, the entire ecosystem is trying to build a closed loop closer to Web2 user habits. On-chain native consumption (including Meme, DePIN, mini-games, community points, social media) has become Solana's "local life", creating natural consumption scenarios for SOL. Although its TVL is only 12% of Ethereum's, Solana's on-chain transaction frequency, per capita interaction, and total Gas consumption have significantly surpassed traditional L1s like Polygon and BNB Chain. It's more like the "daily active entry" for crypto natives, rather than a pure financial "pricing anchor".

Price Signal: Breaking Through $200, Entering High Volatility Main Uptrend:

With BTC stabilizing at $120,000 and ETH sprinting to $4,000, SOL has recently returned above $200. High volatility accompanied by high heat is itself a precursor to new narrative brewing and main position changes. What we're seeing is not speculative frenzy, but an increasingly shorter feedback loop between "on-chain behavior-price reaction".

This is a model driven by consumer data to drive trading expectations, which ETH cannot do, making SOL the paradigm.

On-chain data shows that since Q2 2025, the "on-chain position building" behaviors of three major institutions have shown completely different strategies:Grayscale continuously increased its ETH holdings from May to July (accumulating 172,000, about $640 million), clearly for its spot ETH ETF base position construction;Jump Trading has frequently adjusted positions on the Solana chain since June, focusing on BONK, PENGU, and Jupiter, and accumulating nearly 280,000 SOL through multiple addresses;Listed companies DeFi Development Corp and Upexi have continuously announced increases in SOL holdings, both forming holdings of over 1 million (total market cap nearly $500 million), with considerable floating profits.

This is not a simple "win or lose" bet, but market stratification: ETH is "structural asset allocation", SOL is "short-cycle volatility tool".

Differentiated Policy Trends Boost "Dual-Line Growth". On July 19, U.S. President Trump officially signed the "U.S. Stablecoin National Innovation Guidance Act (GENIUS Act)", the first federal regulatory framework for stablecoins in the U.S., coupled with Coinbase and BlackRock submitting S-1 spot ETH ETF documents, the path for "ETH incorporation into compliance frameworks" is becoming clearer. At the same time, the Solana team is collaborating with exchanges like OKX and Bybit to advance "consumer asset compliance issuance" experiments. For example, OKX launched a Solana on-chain asset exclusive Launchpad in July, introducing light KYC mechanisms for Meme coin issuance processes.

This "two-way compliance" means policy dividends are being distributed differently based on application scenarios, capital attributes, and risk preferences: ETH continues to absorb traditional capital, SOL becomes a compliant testing ground for young users and consumer scenarios.

Short-term Policy Expectations: ETH Benefits More Clearly, SOL Faces Fewer Restrictions. Although ETH is at the forefront of policy dividends in ETFs and RWA, it also faces multiple thresholds from the SEC in terms of security attribute determination and staking classification. The SOL ecosystem, because it is less involved in centralized issuance and complex staking channels, finds its tokens and applications easier to enter the regulatory "gray safe zone". This leads to ETH's upward path being more stable but longer in cycle, SOL's upward path being steeper and more volatile.

SOL is the Short-Term Explosive Device in Structural Cracks

Compared to ETH's stability, SOL has become the main battlefield for capital games in high-frequency trading, Meme coin narratives, terminal applications, and native consumer goods (like the Saga phone). From BONK to PENGU, to JUP's governance experiments, the Solana chain has built a high-liquidity, high-penetration "native narrative market".

Combined with on-chain performance: SOL's TPS, costs, and terminal response speed continue to lead; and the independence of the SVM ecosystem has freed it from the internal competition and redundant construction of the EVM ecosystem.

More importantly, SOL is one of the few "narrative depressions" capable of承接资金且愿意高波动, becoming the core short-cycle option to capture "quick reactions to capital rotation" after BTC starts its main uptrend.

Therefore, this is not a "multiple-choice question", but a "cycle game question":

For medium-to-long-term capital看好制度变革、押注传统资本结构化进场, ETH is the首选. For短周期参与者希望捕捉资金轮动与叙事爆发机会,SOL provides more张力 Beta exposure.

Between narrative and institution, volatility and sedimentation, ETH and SOL may no longer be对立 options, but构成一个时代错配下的最优组合.

谁定义未来?目前看来,答案或许并非单一项目,而是这个"组合权重"的持续微调过程.