In-depth Research Report on Stock Tokenization: Unlocking the Second Growth Curve of the Bull Market

分享到朋友或朋友圈

1. Introduction and Background

Over the past year, the concept of tokenizing real-world assets (RWA) has gradually moved from the fringe narrative of fintech to the mainstream view of the crypto market. Whether it's the widespread application of stablecoins in the field of payment and clearing, or the rapid growth of on-chain treasury bills and note products, the "tokenization of traditional assets" has transformed from an idealized vision into a real-world experiment. In this trend, tokenized stocks, known as "on-chain U.S. stocks," have become one of the most controversial and potentially promising tracks. What they carry is not only an attempt to reform the liquidity and trading timeliness of traditional securities markets but also challenges to regulatory boundaries and the opening of cross-market arbitrage spaces. For the crypto industry, this could be a generational leap that introduces a trillion-dollar asset pool into the on-chain world; for traditional finance, it's more like an "unauthorized" technological breakthrough, bringing both an efficiency revolution and potential governance conflicts.

2. Market Status & Key Paths

Although "tokenization" has become one of the most important mid-to-long-term narratives in the crypto industry, when it comes to the specific asset class of "stocks," progress remains slow, with significant divergence in paths. Unlike standardized assets such as treasury bills, short-term notes, and gold, the tokenization of stocks involves more complex issues of legal ownership, trading timeliness, voting rights design, and dividend distribution mechanisms. This has led to a clear division in the market among several products in terms of compliance paths, financial structures, and on-chain implementation methods.

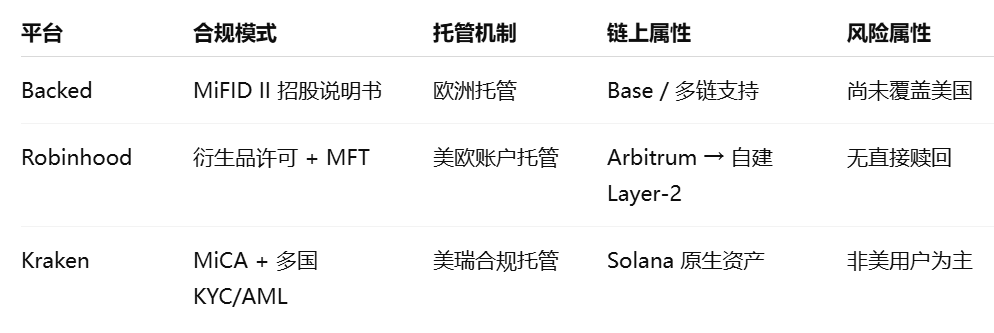

One of the projects that achieved early results in this field is Backed Finance. This Swiss-based fintech company, in collaboration with regulated securities custodians, has launched several ERC-20 tokens backed by real stocks and ETFs, attempting to build an "intermediate bridge for on-chain securities." Taking its well-known product wbCOIN as an example, the token claims to be 1:1 pegged to Coinbase's real stock on NASDAQ, with custodians Alpaca Securities and InCore Bank promising redeemability for real stocks, theoretically possessing a closed-loop logic of "subscription—holding—redemption." Backed has also launched tokens for NVIDIA (BNVDA), Tesla (BTESLA), S&P 500 ETF (BSPY), and others, using chains like Base and Polygon as circulation carriers to provide investors with on-chain trading entry points. However, there is still a gap between ideal and reality. As of March 2025, the total TVL of Backed's multiple tokenized stock products has not exceeded $10 million, with wbCOIN's daily trading volume even falling below $4,000, and trading records in most periods approaching zero. The reasons for this situation are not singular, including early users' uncertainty about the redemption mechanism, the DeFi ecosystem's failure to fully integrate these tokens, and some on-chain market makers' judgment that such assets "lack long-term liquidity expectations." This means that even if the product mechanism has achieved clarity in asset mapping and completeness in the custody chain, the lack of trading depth, usage scenarios, and user awareness may still leave tokenized U.S. stocks in a "compliant but deserted" predicament.

Compared to Backed, Robinhood's tokenization path appears more conservative but systematically stronger. As a platform that has long been cautiously laying out its crypto business, Robinhood chose to launch regulated stock derivative tokens in the EU region. These tokens do not essentially map to real stocks but are price-tracking derivative tools based on the EU's MFT (Multilateral Trading Facility) license. The logic behind this is closer to traditional CFDs (Contracts for Difference), where traders do not actually hold the underlying stocks but hold rights and obligations to price fluctuations. Although this design sacrifices the on-chain purity of "1:1 anchoring to real stocks," it significantly reduces regulatory conflicts and custody complexity, achieving a compromise solution of "non-securities but tradable." Robinhood provides complete UI support, asset splitting, dividend distribution, leverage settings, and other services, and ensures user rights through its own custody account system; more importantly, its future plan to launch a Layer 2 network (temporarily named Robinhood Chain) also means that Robinhood is embedding tokenized stocks into its native wallet and crypto trading platform in an "application chain" manner. This top-down constructed closed-loop ecosystem may be more suitable for new users to get started, but it also limits the openness of asset circulation, and currently, trading times are still restricted to the opening hours of European financial markets, with insufficient on-chain nativity.

In contrast, the xStocks ecosystem launched by Kraken and its partners offers another path of imagination. This solution is based on the Solana chain, with Backed providing the underlying asset tokens, bypassing U.S. regulation through structured compliance methods and opening the product to global non-U.S. markets. The most distinctive feature of xStocks is its "DeFi-ization" of trading attributes: all tokens can be traded 24/7, with T+0 settlement, on-chain swaps, and stablecoin market-making functions, theoretically capable of integrating into existing DeFi toolchains such as lending, perpetual contracts, and cross-chain liquidity bridging. The system also attempts to aggregate trading depth through on-chain liquidity pools and has established initial connections with Solana-native DEXs like Orca and Jupiter. This on-chain native, globally distributed, and composable attribute undoubtedly represents the "ultimate vision" of tokenized stocks, not just as price-mapping products but as building a truly integrated cross-market of traditional financial assets and crypto infrastructure. However, xStocks' current biggest challenges still lie in limited user coverage, the need for KYC review for real subscription/redemption, and the unresolved question of whether its custody path has transnational legal effect. Additionally, although its trading experience and mechanisms have reached "crypto-native" standards, the actual user scale and on-chain liquidity have not yet formed a scale effect, with a long way to go before mainstream adoption.

From the layout differences of these three, it can be seen that there is currently no unified standard for stock tokenization, but each designs its path based on its own advantages, regulatory environment, and ecosystem resources. Among them, Robinhood emphasizes "regulated traditional trading experience plus crypto packaging," Backed emphasizes "on-chain tool contracts mapping real assets," and Kraken is more inclined to "build a crypto-native liquidity market." The different paths of the three not only demonstrate the diversity of this track but also reveal the typical characteristics of an immature market: among compliance, asset mapping, and user needs, no one can achieve comprehensive coverage, and ultimately, it still requires time and market feedback to eliminate and filter.

It can be said that tokenized stocks are still in a very early experimental stage. Although they have a theoretical closed loop, their on-chain activity and financial efficiency are still far below expectations. Their future development key not only depends on whether the product design itself is perfect but also on whether three major elements can converge: first, whether more real liquidity participants can enter their trading pools to form a price discovery mechanism; second, whether they can integrate into richer DeFi applications to enhance the usage scenarios of tokenized stocks; third, whether regulations can gradually clarify red line boundaries, giving platforms the confidence to expand service coverage, especially to U.S. users. Before these paths are completed, tokenized stocks are more like a financial experiment with great potential than a growth engine that can fulfill bull market expectations at this stage.

3. Compliance Mechanisms and Implementation Capabilities

In all discussions about tokenized stocks, regulation is always the sword of Damocles hanging overhead. As one of the most tightly regulated financial assets, stocks are strictly constrained by the laws of their jurisdictions in every aspect of issuance, trading, custody, and clearing. In traditional finance, securities must be registered or exempted to be legally sold, and trading venues also need to obtain relevant licenses such as exchanges or ATS (Alternative Trading Systems). Reconstructing these securities as "on-chain assets" means not only solving the problem of technical mapping but also connecting to clear and executable compliance paths. Otherwise, even with excellent product design, it is difficult to break through the limitations of usage scope, inability to promote to qualified investors, and even the legal risks of potentially touching illegal securities issuance. In this regard, the choices and differences of different projects are particularly distinct, which precisely determines whether they can truly move towards large-scale implementation in the future.

Taking Backed Finance as an example, it has adopted the approach closest to the "traditional securities issuance logic" in its compliance path. The stock tokens issued by Backed essentially belong to restricted securities recognized by Swiss regulators, meaning that token purchasers must complete KYC/AML reviews and promise not to sell to U.S. investors, while secondary market circulation is also restricted to "qualified investors only." Although this method is relatively robust in compliance, avoiding touching the red lines of the U.S. SEC, it also brings problems of limited circulation, unable to realize the vision of free trading of tokens on public chains. A more practical challenge is that this "restricted securities" model requires every transfer to undergo compliance verification, greatly weakening its composability with DeFi systems. In other words, even if Backed has successfully established a custody mapping relationship between tokens and real stocks with InCore Bank and Alpaca Securities, what it has built is still a closed ecosystem within a "regulatory sandbox," difficult to achieve high-frequency trading, collateral, leverage, and other applications in open financial scenarios.

The path adopted by Robinhood is a more clever compliance packaging. Its tokenized stock products do not directly map to real stocks but are "security derivatives" constructed under the EU MiFID II regulatory framework, technically similar to CFDs (Contracts for Difference), and provided with quotation, custody, and clearing support by its regulated subsidiaries. This design allows Robinhood to avoid the legal responsibility of directly holding stocks and also circumvents the problems of peer-to-peer trading and physical delivery, thus enabling the provision of related product trading without possessing a securities license. The advantage of this path is its high compliance certainty, allowing for the rapid launch of multiple underlying stock tokens and promotion through its existing user system; but the cost is that the assets themselves lack programmability and openness, unable to truly embed into on-chain native financial protocols. Further, this "platform custody + derivative tracking" model essentially still belongs to the CeFi (Centralized Finance) category, with the issuance and clearing of assets almost entirely dependent on the Robinhood system's internal realization, and users' trust in the underlying assets still based on trust in the platform, not on-chain autonomous custody and verification mechanisms.

In the case of Kraken and xStocks, we see a more radical, fundamentalist-style compliance treatment. The tokenization mechanism behind xStocks is technically supported by Backed, but in circulation and use, it takes a gray compliance path of "on-chain autonomy + global non-U.S. user access." Specifically, this model utilizes the "restricted securities + non-public offering" exemption clause in Swiss law, allowing Kraken to open its tokenized products to global non-U.S. markets for trading and restricting access from U.S. IPs through on-chain contracts. This method not only avoids direct scrutiny from the SEC and FINRA on securities issuance and exchange regulation but also retains the characteristic of free circulation of tokens on-chain, enabling them to connect to DeFi lending protocols, AMM market-making, cross-chain bridges, and other modules, forming a relatively complete financial closed loop. However, the risk of this path lies in its extreme reliance on the technical isolation of "non-U.S. user identities." Once a large number of users bypass the restrictions, it may still be considered as "providing illegal securities to U.S. investors," triggering enforcement risks. Moreover, U.S. regulators' determination of "de facto market participation" is often not limited to the setting of technical barriers but based on behavioral consequences and the actual nationality of investors, meaning that even if Kraken tries its best to avoid it, it may still face potential threats of regulatory spot checks or even sanctions.

More macroscopically, currently, whether it's Backed, Robinhood, or Kraken, none of their tokenized stock solutions have achieved truly global compliance coverage, but rather a strategy of "regional arbitrage + operation within legal gaps." The fundamental reason for this situation is the significant differences in the definition of securities nature across countries. Taking the U.S. as an example, the SEC still considers "any token pegged to the value of real equity" as a security, and its issuance must meet the Howey Test or pass compliance exemptions such as Reg A / Reg D. The EU is relatively lenient, allowing some derivative-structured tokens to be traded under the jurisdiction of MTF or DLT Pilot Regime; as for countries like Switzerland and Liechtenstein, they attract project parties to conduct pilot issuances through sandbox regulation and dual registration systems. This regulatory fragmentation creates a huge space for institutional arbitrage and also presents the implementation of tokenized stocks as a situation of "regional compliance, global gray areas."

In this complex context, the future large-scale implementation of stock tokenization will inevitably rely on breakthroughs in three aspects. First is the unification of regulatory cognition and the establishment of exemption channels, requiring the design of a legal and replicable compliance template for tokenized securities, similar to the EU's MiCA, the UK's FCA sandbox, and Hong Kong's VASP systems. Second is the native support of on-chain infrastructure for compliance modules, including the standardization of tools such as KYC modules, whitelist transfers, and on-chain audit trails, to enable compliant securities to truly embed into the DeFi system, rather than becoming liquidity islands. Third is the entry of institutional participants, especially the collaborative cooperation of financial intermediaries such as custody banks, audit firms, and brokers, to solve the problems of asset authenticity and redemption mechanism credibility.

It can be said that compliance mechanisms are not subsidiary issues of stock tokenization but key variables of its success or failure. No matter how decentralized a project is, its foundation is still built on the logic of "whether real assets can be credibly mapped"; and the core issue behind this is always whether the legal framework can accommodate the existence of new paradigms. Therefore, when studying tokenized stocks, we should not only focus on mechanism innovation and technical architecture but also understand the boundaries and compromises of institutional evolution, finding a feasible middle path between regulatory reality and on-chain ideals.

4. Market Analysis and Future Outlook

The total amount of global RWA (Real World Assets) on-chain is about $17.8 billion, with stock assets only accounting for $15.43 million, merely 0.09% of the total scale. However, tokenized stocks have grown more than threefold in half a year, from $50 million in July 2024 to ~$150 million in March 2025.

When we re-examine the actual performance of the tokenized stock track, it is not difficult to find that it has both strong conceptual appeal and extremely complex real-world implementation barriers. From a theoretical logic perspective, stock tokenization has obvious structural advantages: on one hand, it maps the most valuable and cognitively foundational real assets onto the chain, bringing real-world credit anchors to the crypto ecosystem; on the other hand, it achieves trading automation and real-time settlement through smart contracts, subverting the fundamental logic of traditional securities markets relying on centralized clearinghouses and T+2 cycles, releasing extremely high system efficiency. However, in practice, these advantages have not yet translated into large-scale adoption, but have long been in an awkward state of "mechanism established, scenarios missing, liquidity dried up." This also forces us to think further: what is the real growth engine of stock tokenization? Could it become a core asset class in crypto finance like stablecoins or on-chain bonds in future markets?

Structurally, the first-order value of stock tokenization lies in "connecting real markets with on-chain markets," but the real incremental demand must come from three types of user groups: first, retail investors who hope to bypass traditional financial institutions and participate in global stock markets with lower thresholds; second, high-net-worth individuals and gray funds seeking cross-border asset flows, evading capital controls or time zone restrictions; third, DeFi protocols and market makers targeting arbitrage and structural returns. These three groups jointly shape the "potential market" of tokenized stocks, but currently, none have truly entered on a large scale. Retail investors often lack on-chain operation experience and lack confidence in the mechanism of "whether they can be redeemed for real stocks"; high-net-worth users have not yet confirmed whether such assets have sufficient privacy protection and hedging attributes; and DeFi protocols are more inclined to build structural products around high-frequency trading, stablecoins, and derivatives, with limited interest in stock assets lacking volatility and liquidity. This means that stock tokenization currently faces a typical market misalignment problem of "financial assets wanting to go on-chain, but on-chain users are not yet ready to accept them."

Even so, future turning points may gradually emerge with several key trends. First, the rise of stablecoins provides a solid monetary foundation for the trading and settlement of tokenized stocks. When stablecoins like USDC, USDT, and PYUSD become the "digital dollars" of on-chain liquidity, stock tokens naturally gain a universal counterparty asset. This allows users to conduct U.S. stock-related transactions without accessing the banking system, lowering entry barriers and capital switching costs, which is particularly important for users in developing countries. Second, the maturity of DeFi protocols gradually builds the ability to combine "on-chain traditional assets." With the emergence of assets like tokenized treasury bills and tokenized money market funds, the market's acceptance of "on-chain non-crypto-native assets" has significantly increased, and stocks are undoubtedly the next standard asset type to be connected. In the future, if an on-chain investment portfolio tool that includes "stocks + bonds + stablecoins" can be formed, it will be highly attractive to institutional users and may even evolve into "on-chain ETFs / index funds" similar to traditional brokers.

Another variable that cannot be ignored is the explosion of L2 and application chain ecosystems. With the expansion of the user base of Ethereum Layer 2 networks like Arbitrum, Base, Scroll, and ZKSync, and the enhancement of financial nativity of high-performance chains like Solana, Sei, and Sui, the "on-chain residence" of stock tokens is no longer limited to isolated asset issuance platforms but can be directly deployed on chains with deep liquidity and developer foundations. For example, if Robinhood's Robinhood Chain successfully embeds the trading data and capital flows of its hundreds of millions of users, combined with the integration of compliant on-chain wallet opening and KYC custody tools, it could theoretically build a hybrid financial model of "centralized user experience + on-chain asset architecture" in a closed-loop ecosystem, thereby promoting the actual usage frequency and financial combination complexity of stock tokens. And projects like xStocks in the Solana ecosystem may also have structural advantages in scenarios such as arbitrage, perpetual contracts, and segmented fixed investments due to their high-frequency trading capabilities and low fee advantages.

At the same time, from the perspective of the macro-financial cycle, the emergence of stock tokenization coincides with a critical stage where global capital markets and crypto markets are beginning to further integrate. With the approval of ETF-ized Bitcoin and RWA gradually becoming the focus of traditional institutions' on-chain layouts, the crypto world is transitioning from an "island economy" to a "global asset-compatible system." In this context, stocks are undoubtedly the most symbolic connection point. Especially when investors begin to seek more flexible, efficient, and 24/7 cross-border allocation tools, "U.S. stocks" in the form of tokens are likely to become the core springboard for global capital flows. This also explains why traditional asset management giants like Franklin Templeton and BlackRock are researching new structures such as security tokens and on-chain investment funds, aiming to pave the way for the next stage of market structural changes in advance.

Of course, in the short term, stock tokenization still cannot escape several realistic constraints. Liquidity remains scarce, user education costs are high, compliance paths are full of uncertainty, and asset mapping mechanisms still have high trust costs. More importantly, there is no "clearly first-mover advantage" leading project, lacking standard-type assets like USDC, WBTC, and sDAI that have become protocol components. This leaves the current market still in the exploration phase, with each project trying to overcome the two major challenges of compliance and usability in different ways, but still needing time and patience to standardize and scale.

However, precisely because of this, stock tokenization may be at a "severely underestimated early starting point." It does not directly assume monetary functions like stablecoins, nor does it have the native network effects of ETH and BTC, but the ability it represents to "map the real world on-chain" is becoming a key piece in connecting the two systems. In the future, projects with truly explosive potential are likely not some new asset but a "compliance integration platform" that can integrate asset custody, trading matching, KYC review, on-chain combination, and off-chain clearing, aiming not to completely replace traditional brokers but to become the "Web3 compatibility layer" of the global financial system. When such a platform has sufficient user volume and infrastructure support, stock tokenization will not just be a narrative but will become a core component of the on-chain capital market.

5. Conclusions and Recommendations

Looking back at the development context of stock tokenization, we can clearly see a typical cyclical phenomenon of "technology first, compliance lagging, market waiting." This technology is not newly invented, nor is it an incomprehensible financial engineering problem; the mechanism logic behind it—mapping real stocks through on-chain assets to give them global, 7×24-hour trading and combination capabilities—has been fully demonstrated in both technical and financial dimensions. But the real problem is not whether the mechanism itself is feasible, but how this mechanism can find a feasible path to take root, sprout, and steadily expand in the complex regulatory context, financial infrastructure, and market inertia of the real world. In other words, the reason why stock tokenization has not yet formed explosive growth is not that it is not "good" enough, but that it is not yet "mature" enough, not "usable" enough, and has not truly hit a strategic node where policy windows and financial needs intersect.

But this situation is quietly changing. On one hand, the acceptance of blockchain by traditional capital markets is rapidly increasing, from BlackRock's on-chain funds to JPMorgan's on-chain settlement network to BlackRock-led Ethereum on-chain RWA infrastructure, all releasing a strong signal: real-world assets are gradually going on-chain, and the future financial infrastructure will no longer be a binary opposition of "traditional vs. crypto" but a fusion middle ground. In this major trend, as one of the most mature real assets, the on-chain mapping value of stocks is naturally significant. On the other hand, the crypto-native ecosystem itself is also transitioning from pure speculation to structural construction. From stablecoins and lending protocols to attempts at on-chain treasury bills and ETFs, users are beginning to demand higher "stability, liquidity, and compliance" from assets, and the stock asset category happens to play a connecting role—representing both the credit cornerstone of the real world and being able to embed into smart contracts and DeFi modules through tokenization, becoming an important part of on-chain investment portfolios.

Therefore, stock tokenization is not just an "interesting narrative" but a mid-to-long-term opportunity track with a real demand foundation, policy game space, and technical implementation path. For industry practitioners, there are several clear recommended directions.

First, when entering the field of stock tokenization, project parties must prioritize "compliance path design" over technological innovation or user experience optimization. The projects that truly have the opportunity to grow big and strong will be those that can construct legal and compliant issuance structures and on-chain trading mechanisms in friendly jurisdictions like Switzerland, the EU, the UAE, and Hong Kong. Technology is only a prerequisite; institutions are the boundaries, and compliance is the moat of growth.

Second, the essence of asset tokenization is "infrastructure-level asset issuance," meaning its value does not depend on whether a certain stock is popular but on whether the entire system can connect to more on-chain protocols and become a standard asset component. Therefore, tokenized stock projects must actively connect with various DeFi protocols to promote the implementation of combined products like "rTSLA collateralized loans," "aAAPL perpetual contracts," and "SPY ETF token re-staking." Otherwise, even with compliance and custody, they can only become "conceptual tools" in low-frequency trading scenarios.

Third, user education and product packaging are equally critical. On-chain stock trading cannot continue to maintain its current high-threshold form that only professional players can understand but should actively learn from platforms like Robinhood, eToro, and Interactive Brokers, introducing familiar UI language, simplified trading processes, and visualized income structures to minimize user entry barriers and truly bring traditional investors into the crypto world. For ordinary users, the logic of being able to buy a share of AAPL with an on-chain wallet is far more attractive than understanding whether the custody structure behind it is based on CSD.

Finally, policy participation and regulatory dialogue must be front-loaded, especially in regions like Hong Kong, Abu Dhabi, and London that are actively promoting RWA policy innovation, to promote the formation of industry self-regulatory organizations, technical standard templates, and pilot regulatory sandboxes. Whether stock tokenization ultimately succeeds does not depend on whether more complex asset packaging structures can be built but on whether policymakers can be convinced that this is a "controllable, incremental, and beneficial financial innovation," not another impact and challenge to the existing financial order.

In conclusion, stock tokenization is a proposition full of tension. It connects the oldest financial assets with the latest technological paradigms, representing a collective demand for "capital flow liberalization" and "financial infrastructure reconstruction." In the short term, it will still be an endurance battle of regulation, cognition, and trust; but in the long run, it may become the "third pillar" in the development process of on-chain finance, following stablecoins and on-chain treasury bills. This is not a hype hotspot but a deep-water area, a direction truly worthy of long-term participation and investment over a 3–5 year cycle. If the basic logic of the next bull market is "on-chain real economy," then stock tokenization is likely to be the most concrete, value-supported, and regulatory-controversial key breakthrough.

For investors & institutions, we recommend considering the following short-term, mid-term, and long-term aspects:

Short-term: Focus on product launch, TVL, market-making mechanisms, on-chain trading data, and regulatory dynamics (such as MiCA, SEC guidance).

Mid-term: Evaluate whether platforms have added perpetual contracts, leverage mechanisms, DeFi support, as well as on-chain indicators like capital costs and liquidity efficiency.

Long-term: Pay attention to whether U.S. users are granted trading permissions, the path to T+0 realization and compliance mechanism integration, and the trend of capital reallocation between on-chain funds and altcoins/new assets.

In summary, U.S. stock tokenization is an "important experiment" in the structural transformation of the crypto market. Although there is no explosive trading volume yet, it is accumulating the underlying foundation for the second round of the bull market. If compliance openness, on-chain depth, and mechanism innovation can converge, this "old bottle with new wine" may become the key engine driving the next wave of growth in the crypto market.